The year-on-year growth of broad money (M2b) indicated some deceleration, recording 18.9 per cent in March 2016, compared to 19.8 per cent in February 2016. The expansion in domestic credit remained the key driver of broad money growth, within which credit extended to the private sector by commercial banks recorded a year-on-year growth of 27.7 per cent in March 2016, compared to 26.5 per cent in the previous month. With regard to sectoral distribution of credit, Industry and Services sectors attracted the highest levels of credit disbursements, while personal loans and advances also recorded a substantial increase. Meanwhile, with the low level of excess rupee liquidity in the domestic money market amid recent monetary tightening measures, an upward movement in short term money market rates and other market interest rates was observed. Reflecting the gradual transmission of increased short term interest rates to broader market interest rates, the expansion of monetary and credit aggregates is expected to moderate from the second quarter of the year.

Headline inflation, as measured by the Colombo Consumers’ Price Index (CCPI, 2006/07=100), was 3.1 per cent, year-on-year, in April 2016 compared to 2.0 per cent in the previous month. Annual average headline inflation based on CCPI edged up to 1.3 per cent from 1.1 per cent in March 2016. However, the CCPI based core inflation remained unchanged at 4.5 per cent in April 2016, on a year-on-year basis, compared to the previous month. Meanwhile, the National Consumer Price Index (NCPI, 2013=100) based headline inflation increased to 2.2 per cent, year-on-year, in March 2016 compared to 1.7 per cent in the previous month, while on an annual average basis, it stood at 2.4 per cent. The recent increase in the Value Added Tax (VAT) rate and the removal of certain exemptions applicable on VAT and the Nation Building Tax (NBT) are expected to have a one-off impact on inflation, while the supply side disruptions due to prevailing adverse weather conditions could exert some upward pressure on inflation in the immediate future. In spite of these temporary disruptions, inflation is expected to remain in midsingle digit levels supported by appropriate demand management policies.

On the external front, the trade deficit registered a contraction of 2.2 per cent on a cumulative basis in the first three months of 2016. Meanwhile, earnings from tourism are estimated to have increased by 20.0 per cent in the first four months of the year while workers’ remittances recorded an increase of 8.1 per cent during the first quarter. Gross official reserves are estimated to have declined marginally to US dollars 6.1 billion by end April 2016 from US dollars 6.2 billion in the previous month while the Sri Lanka rupee has recorded a marginal depreciation thus far during 2016. Meanwhile, a renewed foreign interest in investments in Government securities has been observed since April 2016 as reflected by net foreign inflows to the Government securities market. Going forward, the Extended Fund Facility (EFF) expected from the IMF and the other multilateral and bilateral credit facilities, along with the planned structural reforms, would enhance the country’s resilience to external shocks and improve investor confidence in the economy.

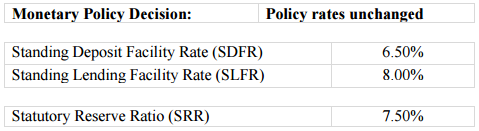

Taking into consideration the developments discussed above, the Monetary Board, at its meeting held on 20 May 2016, was of the view that the current monetary policy stance of the Central Bank is appropriate. Accordingly, the Monetary Board decided to maintain the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) of the Central Bank unchanged at 6.50 per cent and 8.00 per cent, respectively.

Headline inflation, as measured by the Colombo Consumers’ Price Index (CCPI, 2006/07=100), was 3.1 per cent, year-on-year, in April 2016 compared to 2.0 per cent in the previous month. Annual average headline inflation based on CCPI edged up to 1.3 per cent from 1.1 per cent in March 2016. However, the CCPI based core inflation remained unchanged at 4.5 per cent in April 2016, on a year-on-year basis, compared to the previous month. Meanwhile, the National Consumer Price Index (NCPI, 2013=100) based headline inflation increased to 2.2 per cent, year-on-year, in March 2016 compared to 1.7 per cent in the previous month, while on an annual average basis, it stood at 2.4 per cent. The recent increase in the Value Added Tax (VAT) rate and the removal of certain exemptions applicable on VAT and the Nation Building Tax (NBT) are expected to have a one-off impact on inflation, while the supply side disruptions due to prevailing adverse weather conditions could exert some upward pressure on inflation in the immediate future. In spite of these temporary disruptions, inflation is expected to remain in midsingle digit levels supported by appropriate demand management policies.

On the external front, the trade deficit registered a contraction of 2.2 per cent on a cumulative basis in the first three months of 2016. Meanwhile, earnings from tourism are estimated to have increased by 20.0 per cent in the first four months of the year while workers’ remittances recorded an increase of 8.1 per cent during the first quarter. Gross official reserves are estimated to have declined marginally to US dollars 6.1 billion by end April 2016 from US dollars 6.2 billion in the previous month while the Sri Lanka rupee has recorded a marginal depreciation thus far during 2016. Meanwhile, a renewed foreign interest in investments in Government securities has been observed since April 2016 as reflected by net foreign inflows to the Government securities market. Going forward, the Extended Fund Facility (EFF) expected from the IMF and the other multilateral and bilateral credit facilities, along with the planned structural reforms, would enhance the country’s resilience to external shocks and improve investor confidence in the economy.

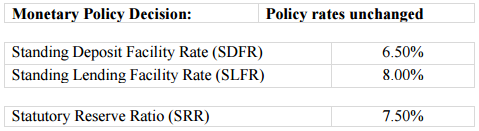

Taking into consideration the developments discussed above, the Monetary Board, at its meeting held on 20 May 2016, was of the view that the current monetary policy stance of the Central Bank is appropriate. Accordingly, the Monetary Board decided to maintain the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) of the Central Bank unchanged at 6.50 per cent and 8.00 per cent, respectively.

No comments:

Post a Comment