According to the provisional estimates of the Department of Census and Statistics (DCS), the Sri Lankan economy is estimated to have grown by 4.1 per cent during the third quarter of 2016 compared to the growth of 5.6 per cent in the corresponding period of the previous year. Services activities grew by 4.7 per cent, while Industry activities grew notably by 6.8 per cent during the third quarter of 2016. However, Agriculture related activities continued to report a contraction, for the second consecutive quarter, by 1.9 per cent, impacted by the adverse weather conditions that prevailed during the third quarter of 2016. Favourable developments in leading economic indicators as well as the lower base in the fourth quarter of 2015 are likely to steer economic growth upwards in the final quarter of 2016 in spite of the effect of adverse weather conditions and global economic uncertainties.

According to the provisional estimates of the Department of Census and Statistics (DCS), the Sri Lankan economy is estimated to have grown by 4.1 per cent during the third quarter of 2016 compared to the growth of 5.6 per cent in the corresponding period of the previous year. Services activities grew by 4.7 per cent, while Industry activities grew notably by 6.8 per cent during the third quarter of 2016. However, Agriculture related activities continued to report a contraction, for the second consecutive quarter, by 1.9 per cent, impacted by the adverse weather conditions that prevailed during the third quarter of 2016. Favourable developments in leading economic indicators as well as the lower base in the fourth quarter of 2015 are likely to steer economic growth upwards in the final quarter of 2016 in spite of the effect of adverse weather conditions and global economic uncertainties.Headline inflation, as measured by the Colombo Consumers’ Price Index (CCPI, 2006/07=100), increased to 4.1 per cent, on a year-on-year basis, in December 2016 from 3.4 per cent in November 2016. In the month of November, headline inflation as measured by the National Consumer Price Index (NCPI, 2013=100), declined to 4.1 per cent, year-on-year, compared to 5.0 per cent in October 2016. Core inflation increased noticeably during December 2016 mainly reflecting the effect of government tax changes. Consequently, core inflation as per the CCPI accelerated to 6.3 per cent (year-on-year) in December 2016 from 5.1 per cent in November 2016, while core inflation based on NCPI increased markedly to 6.8 per cent in November 2016 from 5.7 per cent in October 2016. Despite these transitory movements, inflation is likely to remain at midsingle digits in the period ahead, on average.

In the monetary sector, year-on-year growth of credit extended to the private sector by commercial banks witnessed the anticipated deceleration, and was 22.0 per cent in October 2016 compared to 25.6 per cent in the previous month. However, the net increase in credit extended to the private sector, in absolute terms, remained high at Rs. 79.0 billion during October 2016. Meanwhile, credit to the public sector from commercial banks increased modestly in October 2016. Accordingly, broad money (M2b) growth decelerated to 17.8 per cent, on a year-on-year basis, in October from 18.4 per cent in September 2016. Rupee liquidity in the domestic money market returned to surplus levels in December, while market interest rates, which increased in response to monetary tightening measures adopted by the Central Bank, appear to have broadly stabilised during the month.

In the external sector, mainly due to the effect of a one-off increase in the expenditure on imports, the deficit in the trade balance increased substantially in October 2016. Earnings from tourism as well as workers’ remittances continued to grow at a healthy pace. Gross official reserves were estimated at US dollars 5.6 billion by end November 2016, while the Sri Lankan rupee has depreciated by 3.6 per cent against the US dollar thus far during the year.

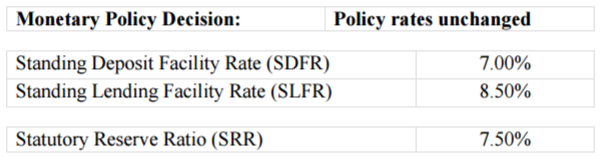

Taking into consideration the developments discussed above, the Monetary Board, at its meeting held on 30 December 2016, was of the view that the current monetary policy stance of the Central Bank is appropriate. Accordingly, the Monetary Board decided to maintain the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) of the Central Bank unchanged at 7.00 per cent and 8.50 per cent, respectively.

No comments:

Post a Comment